Gartner’s view of the market is focused on technologies and approaches delivering on the future needs of end users, not only the market as it is today.

Gartner defines contact center as a service (CCaaS) as solutions offering SaaS-based applications that enable customer service departments to manage multichannel customer interactions holistically from both a customer-experience and employee-experience perspective.

CCaaS solutions offer an adaptive, flexible delivery model with native capabilities across the four functional components of the technology reference model for customer service and support (see Quick Answer: What Does a Technology Reference Model for Customer Service and Support Look Like?). CCaaS providers also offer productized integrations with partner solutions through application marketplaces.

The core functional components of a CCaaS solution are:

● Contact routing and interactions — Focusing on delivering a channel-agnostic, architected design to create customer service journeys, including intelligent self-service. Services are consumed on a per seat, per concurrent user or consumption basis.

● Resource management — Developing and maintaining engaged and empowered staff based on the understanding that engaged employees power a stronger customer experience.

The optional functional components of a CCaaS solution are:

● Process orchestration — Supporting increasingly complex and personalized customer engagements.

● Knowledge and insight — Delivering customer and operational insights and recommending next best actions across all functional groupings.

CCaaS solutions are used by customer service and telemarketing centers, employee service and support centers, help desk service centers, and other types of structured communications operations. CCaaS is now the go-to technology for most organizations looking to procure or replace traditional on-premises contact center technologies. CCaaS solutions are also starting to be deployed in multithousand-seat environments, even though these may comprise multiple smaller entities. This reflects the desire of customer service organizations to consolidate multiple stand-alone environments and move forward with a single, strategic supplier, preferably in the cloud. CCaaS solutions are typically deployed as an integral part of a broader customer service and support technology ecosystem.

There is significant market hype on the impact of AI, particularly generative AI, on the future of CCaaS. While transformation is possible, the technology is nascent, with many services still in trial modes. In addition, the market must work out numerous issues in security, regulations and compliance before wide-scale adoption can occur. Hence, it would be premature to imply that generative AI is having a meaningful impact on CCaaS deployments at the time of this writing. But, GenAI is expected to see adoption in some use cases, such as agent assist and process automation, over the next 12 months.

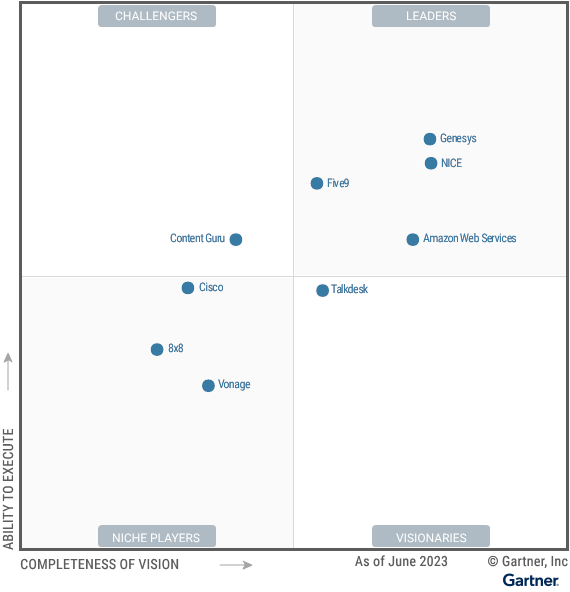

Figure 1: Magic Quadrant for Contact Center as a Service

8x8 is a Niche Player in this Magic Quadrant. Its 8x8 Contact Center is delivered via the 8x8 eXperience Communications as a Service Platform, which integrates CCaaS, UCaaS and CPaaS. It is offered as part of the X Series licensing suite, which includes CCaaS and UCaaS communications as a bundled offering. 8x8 Contact Center is also available as a stand-alone solution. 8x8 has a strong global footprint as a result of its leadership in the UCaaS market. In the last year, 8x8 has improved its CCaaS support for digital channels, AI-enabled self-service, and reporting and analytics capabilities, among others. Its sweet spot for CCaaS are midsize businesses and enterprises looking for a single platform for CCaaS and UCaaS, as well as a Teams-integrated contact center. But it can also meet the needs of large enterprises in environments that do not require a great deal of sophisticated advanced functionality for complex deployments.

Strengths

8x8 can provide CCaaS, UCaaS and CPaaS on a single platform, and is well able to integrate natively with 8x8 Voice for Microsoft Teams, a direct-routing solution.

8x8’s global presence as a UCaaS provider enables it to meet the needs of organizations’ contact center users in multiple regions, particularly where there is a requirement to support both UCaaS and CCaaS.

Customers indicate that 8x8’s agent and supervisor UIs are easy to use.

Cautions

8x8’s sweet spot is midsize contact centers, typically those with fewer than 300 agents. Prospective customers with large customer service requirements should check that 8x8’s feature set will meet the needs of their customer services business unit.

Some clients indicate that 8x8’s reporting capabilities lack the granularity and flexibility expected by large customer service organizations.

8x8 focuses on selling its CCaaS capabilities along with UCaaS, but much of this business comes through third-party sales channels, not all of which have strong contact center expertise.

Amazon Web Services (AWS) is a Leader in this Magic Quadrant. Amazon Connect draws on the broader infrastructure and software capabilities of AWS. It is sold both directly and through an expanding set of large channel partners, notably Salesforce (following its 2020 launch of Service Cloud Voice, which embeds Amazon Connect). Amazon Connect was launched in 2017, and has continually added capabilities to enable it to be a fit in even very large contact center environments. In the last year, Amazon Connect has introduced new functionality such as agent step-by-step guidance; case management; and workforce management (WFM) with agent scheduling, evaluation and screen recording. Amazon Connect sells into businesses of all sizes, from startups to very large global businesses, but especially customers who use AWS as part of an agile development strategy for service delivery.

Strengths

Amazon Connect can be a fit for organizations that prefer to build customized solutions for customer service, either with in-house developer skills or through a network of development partners that can deliver turnkey solutions using the platform.

Amazon Connect’s consumption-based pricing approach is the most agile in the CCaaS market. It enables organizations to experiment with voice, chat and self-service at a low cost without long-term commitments, and clients don’t have to pay for unused capability or seats.

AWS draws on the global reach of its cloud infrastructure and consulting and resale partners to deliver global solutions with very high levels of availability.

Cautions

Organizations that need to extend or customize Amazon Connect beyond its native capabilities and maintain those customizations might choose to hire developers trained on AWS development tools, or engage AWS’ professional services or a certified partner. This can add to the total cost of ownership (TCO) of the deployment.

Some clients indicate that Amazon Connect’s reporting capabilities within the UI lack the granularity and flexibility they require. Some find that they must export data to third-party analytics tools for improved data visualization.

Amazon Connect’s consumption-based pricing requires that organizations understand and can forecast contact volumes to ensure they can predict their TCO across Amazon Connect’s “pay as you go” services.

Cisco is a Niche Player in this Magic Quadrant. Its Webex Contact Center is a CCaaS platform offered to customers through direct and indirect channels. Webex Contact Center was launched in 2020 and is now available globally. Functionality added to Webex Contact Center in the last year includes expanded capacity to support up to 20,000 agents, agent automation capabilities, and support for both Cisco- and third-party-provided AI integration. Webex Contact Center is gaining most traction with midsize contact centers, including those consolidating multiple Cisco Contact Center eXpress on-premises systems, although it is occasionally sold to larger contact centers.

Strengths

Cisco’s Webex Contact Center offers good functionality across a breadth of capabilities, including resource management, analytics and a growing number of technology ecosystem partners.

Webex Contact Center can be deployed with tight integration to Cisco’s collaboration portfolio (UCaaS) and Webex Connect (CPaaS).

Cisco has expanded its support for digital channels through the integration of functionality accessed as part of its 2021 acquisition of imimobile.

Cautions

Organizations planning to leverage a breadth of functionality from Webex Contact Center may find that they must access multiple nonintegrated application development tools for capabilities beyond call routing, such as digital routing, outbound dialer and workforce engagement management (WEM).

Webex Contact Center is based on a different platform and does not offer the same feature set as Cisco’s legacy on-premises products. This creates challenges for customers of Cisco’s legacy contact center products who expect a seamless migration.

The standard service agreement offered for Webex Contact Center is weaker than those offered by most other vendors in this Magic Quadrant. Organizations considering Webex Contact Center should engage in comparative service-level agreement (SLA) evaluations and be prepared to negotiate more meaningful penalties for system downtime.

Content Guru is a Challenger in this Magic Quadrant. Its storm CONTACT is a specialized CCaaS platform offered to customers through direct and indirect channels. Since launching in the U.K. in 2005, Content Guru has extended its footprint mostly in Europe, although it also has a limited presence in North America and Asia/Pacific. In the last year, Content Guru has added functionality to its offerings such as enhancements to its conversational AI, WFM and customer journey management capabilities, among others. Content Guru’s vision focuses on large organizations with deep integration and customization needs, particularly multinational organizations with headquarters in Europe. The company does, however, also have a storm LITE offering for small and midsize businesses (SMBs).

Strengths

Content Guru’s storm CONTACT offering is a highly scalable cloud platform that offers broad integration and automation capabilities through the storm FLOW service builder portal.

Content Guru has extensive experience of meeting the customer service needs of large and complex deployments.

Content Guru has strong references for environments with stringent system resiliency requirements, including those providing emergency medical services requiring 100% system uptime.

Cautions

Most of Content Guru’s operations are centered in Europe. Support in other regions is limited, a shortcoming that requires many organizations to invest more in managing their relationship with the vendor.

Content Guru is frequently less transparent regarding SLAs than many other vendors on this evaluation. Organizations considering storm should engage in comparative SLA evaluations and be prepared to negotiate more meaningful penalties for system downtime.

Gartner clients indicate that it can be challenging to understand the complexity of storm CONTACT’s “a la carte” licensing components and their charges, which add to the TCO.

Five9 is a Leader in this Magic Quadrant. Its Intelligent Cloud Contact Center is offered to enterprises through a dedicated sales team, and the company has increased efforts to sell and support solutions through systems integrators and other channel partnerships. Five9 has more than 20 years’ experience in the CCaaS market. In the last year, Five9 has added functionality to its offering such as expanded capacity to support 10,000+ agents per domain, the ability to link domains for virtually unlimited capacity, enhancements to its digital channels offering and improved agent assist capabilities, among others. With its multiregion platform footprint and growing sales presence, Five9’s execution favors organizations of all sizes in the Americas, including U.S. multinational organizations, with increasing capability to support organizations in other geographic regions.

Strengths

Five9 is building competencies in AI and natural language understanding (NLU) sales and deployments, with increased ability to provide customer references for these functionalities across a variety of vertical markets and use cases.

Five9’s customers frequently praise the company for providing strong postsale support, which helps them derive full value from their investment.

After historically selling primarily to midsize contact centers, Five9 is now regularly deploying its platform in contact centers with hundreds or thousands of agents.

Cautions

Five9’s international growth has, historically, come from its strategy of extending service for U.S.-headquartered customers. Some organizations that choose Five9 may find that service and support requires greater internal investment or reliance on certified partners to manage the supplier relationship than is the case with some alternative vendors.

Some Five9 customers have indicated dissatisfaction with the functionality of its digital interactions and digital self-service.

The standard SLA offered by Five9 is weaker than those offered by most other vendors in this Magic Quadrant. Organizations considering Five9 should engage in comparative SLA evaluations and be prepared to negotiate more meaningful penalties for system downtime.

Genesys is a Leader in this Magic Quadrant. Genesys Cloud CX is a specialized CCaaS platform offered to organizations through a mix of direct sales and channel partner relationships, which vary among regions. Genesys was founded in 1990 and has since established a global sales, marketing and operations presence. It has been successful at using this business foundation to sell and support Genesys Cloud CX, which it launched in 2015. In the last year, Genesys has added functionality to its offering such as enhancements to its support for digital channels, customer journey analytics, and work item and task routing, among others. Genesys Cloud CX can be a fit for organizations of all sizes and geographic requirements, particularly those valuing customer service analytics, AI and automation.

Strengths

Genesys has an extensive operational and channel presence in multiple regions. This wide geographic reach makes it a strong contender for consideration by organizations interested in contact center platform consolidation.

Genesys offers strong tools and processes to migrate customers either from other Genesys offerings or from competitors’ premises-based platforms to Genesys Cloud CX.

Genesys’ strong revenue growth enables the company to fund further growth, R&D and acquisitions to deliver on its strong vision for the evolution of CX management.

Cautions

Some Genesys Cloud CX customers have reported challenges with its native reporting and analytics. They find that they need to work with Genesys AppFoundry partners or Genesys Expert Apps to overcome these challenges.

Some Genesys Cloud CX customers have reported frustration in working with Genesys’ support staff.

Gartner finds that some Genesys Cloud CX customers express that the inability to mix and match major pricing bundles adds to the overall cost of the solution, when in fact adding features to lower-tier licenses may achieve the desired effect. Those considering Genesys Cloud CX should challenge the need for higher-tier licenses if they are not required for all agents.

NICE is a Leader in this Magic Quadrant. CXone, its specialized CCaaS platform, is offered both directly and through a channel program that involves international partners. In the last year, NICE has added functionality to its offering such as advanced routing capabilities, integrating generative AI with Enlighten for consumer and agent guidance, and enhancements to its dedicated real-time supervisor application, among others. NICE CXone appeals to organizations of all sizes and geographic locations that value a strong vision for customer service analytics, workforce engagement, AI and automation.

Strengths

NICE’s Enlighten AI capability draws on the company’s vast amounts of labeled data about customer intents and actions, gained through its WEM interactions captured and embedded across CXone, to build and refine self-learning customer interaction models. The capability also provides conversational guidance for customers, employees and managers. This capability can quickly discover and proactively execute AI-driven customer journeys and workflows.

NICE has a strong vision for supporting end-to-end digital-first journeys, including use of search engine optimization analytics to help optimize digital self- and assisted-service experiences.

NICE can provide consulting services for its CXone offering to a wide range of customer sizes and vertical markets.

Cautions

NICE’s CCaaS offering includes a full cloud-native suite with WEM capabilities. NICE also offers optional specialized best-of-breed WEM capabilities, not fully integrated into the CXone platform but that can be added to it. In some cases, these best-of-breed capabilities may require additional resources to manage, if chosen. Prospective CXone customers should ensure they understand the service proposition differences of NICE’s best-of-breed products.

Some large NICE CXone customers have expressed dissatisfaction with user training materials for the system.

Some Gartner clients who have experience working with NICE’s legacy WEM organization have been hesitant to consider CXone because of poor experiences with NICE’s sales and support. Prospective CXone customers should be aware, however, that CXone-related operations generally do not pose the same challenges — indeed, customers generally express satisfaction.

Talkdesk is a Visionary in this Magic Quadrant. CX Cloud, the vendor’s specialized CCaaS platform, is offered both directly and through channel partners. Founded in 2011 in Portugal and incorporated in the United States, Talkdesk focused initially on the U.S. market before investing further in international expansion. Over the last year, Talkdesk has introduced enhancements to its CX Cloud functionality such as expanding its vertical market products and improving digital interaction routing and agent assist capabilities, among others. Talkdesk has a strong service proposition for multiregion organizations headquartered in North America or Europe.

Strengths

Talkdesk continues to achieve strong customer growth, fueled by innovative functionality and attractive prices.

Talkdesk offers prepackaged industry-specific products for key vertical markets, including banking, insurance, healthcare and retail. These provide deep integration with core systems, applications and workflows at the industry level.

After historically selling primarily to midsize contact centers, Talkdesk is increasingly deploying its platform in contact centers with hundreds or thousands of agents.

Cautions

Although Talkdesk has platform capability in multiple regions, its sales and support organizations are primarily based in the U.S. and Europe. Organizations with users outside these regions should ensure that there is adequate support for their needs.

Despite Talkdesk selling more frequently into larger contact centers than it had previously, most customer reviews of Talkdesk CX Cloud on the Gartner Peer Insights platform are from businesses with annual revenue of less than $1 billion. Prospective customers migrating from a large-scale legacy environment must validate the skill level of the implementation and support teams they will be working with, along with ensuring that system functionality meets their needs.

In the face of strong growth in the Talkdesk customer base, some of its clients have reported challenges in working with the company’s support organization.

Vonage is a Niche Player in this Magic Quadrant. In July 2022, Ericsson, the Swedish telecom equipment manufacturer, acquired Vonage as a wholly owned subsidiary that continues to operate under the Vonage brand. Vonage Contact Center (VCC) is part of a broad “programmable communications platform” strategy incorporating UCaaS, CCaaS, conversational commerce and CPaaS capabilities. VCC was established via Vonage’s acquisition of NewVoiceMedia — a U.K.-based CCaaS provider — in 2018. Over the last year, Vonage has introduced several new capabilities to its VCC offering, such as enhanced integrations to Salesforce and other CRM systems, digital routing and its virtual assistant offerings, among others. Consistent with other UCaaS players, Vonage’s vision is for an integrated platform to meet a broad spectrum of its customers’ communications requirements, not just customer service needs.

Strengths

VCC has an integrated user and administration interface. Customers consistently give it very high ratings on the Salesforce AppExchange.

Vonage continues to improve its support for digital channels. Analytics capabilities help make its offering more interesting to increasingly sophisticated contact centers.

VCC can be deployed with tight integration to Vonage’s collaboration portfolio (UCaaS) and API toolkit (CPaaS), in addition to being able to integrate to Microsoft Teams UCaaS.

Cautions

Some users indicate that Vonage’s support for contact center capabilities outside Europe is weak. Organizations with operations in the Americas and Asia/Pacific may need to invest more resources in managing service issues if they choose Vonage.

Some VCC customers have reported challenges with its native reporting and analytics.

Vonage’s all-encompassing programmable communications platform approach is unlikely to resonate with customer service and support technology leaders. Before choosing Vonage, they should ensure they are sufficiently confident that Vonage will maintain its focus on the CX.

We review and adjust our inclusion criteria for Magic Quadrants as markets change. As a result of these adjustments, the mix of vendors in any Magic Quadrant may change over time. A vendor's appearance in a Magic Quadrant one year and not the next does not necessarily indicate that we have changed our opinion of that vendor. It may be a reflection of a change in the market and, therefore, changed evaluation criteria, or of a change of focus by that vendor.

No vendors were added to this Magic Quadrant.

No vendors were dropped from this Magic Quadrant.

To qualify for inclusion, providers need to fulfill all of the following requirements:

A minimum of $60 million total revenue as of 31 December 2022, composed of concurrent licenses, named user licenses and application consumption. This revenue stream is restricted to enterprise customers and does not include business process outsourcing (BPO) or contact center outsourcing business. We require a letter of attestation from an appropriate finance executive certifying that the minimum revenue requirements are met.

Demonstrated sales, marketing and operational (including company registration) presence in three of the following geographic regions:

North America

Europe

South America (including Central America)

Asia/Pacific

Middle East and Africa

Services should primarily be offered on multitenant platforms and on multiple instances of microservices software as required to meet the needs of customers across several geographies. (Multitenant software describes how the service provider operates a single software instance on which multiple customers can be supported.) To be included in this Magic Quadrant, vendors need to show how their CCaaS platform is designed to support organizations with customer service teams from 25 users up to many thousands of users. The platform must also be able to support both voice and nonvoice channels. This must be evidenced in the vendor’s strategic intent for the CCaaS platform, contract reviews evaluated by Gartner analysts and analysis of company size in Gartner Peer Insights and Gartner Digital Markets platforms. CCaaS providers need to demonstrate how, irrespective of architecture employed, their software inherently provides all customers with transparent access to the same set of services irrespective of location. Software updates must be simultaneously “pushed” to all customers regardless of location, avoiding the traditional “major upgrade” cycles typical of on-premises or single-tenant hosted/managed deployments.

Contact center seat license ownership must be retained by the service provider. Customer contracts must allow for elasticity of usage (enabling customers to scale agent licenses or consumption up or down as usage demands change).

At least 50% of CCaaS service revenue must be from inbound voice agent licenses (automatic call distribution [ACD]). Other licenses may include outbound voice (predictive, progressive or preview dialing) and must include routing of digital interactions (including email, web chat, SMS, social media, video or other channels). They may also include interactive voice response (IVR)/voice portal, WEM, call and/or desktop recording and analytics, knowledge management, workflow routing of noninteraction work items, integration with customer tracking (CRM) and other enterprise databases, and real-time and historical tracking and analytics. The service must provide prepackaged agent, supervisor and reporting applications, although these environments may be extended using a GUI-based interface or open APIs.

Gartner’s definition of CCaaS excludes:

Hosted contact center services, in which system hardware and software are dedicated to individual customers.

Managed services, in which hardware and software are dedicated to a particular customer and run on that customer’s premises or in a third-party data center, but are managed by a third-party service provider.

Enterprise server software repurposed as CCaaS offerings.

Product or Service: The product platform should include the ability to offer (on a subscription basis) all contact center services expected in a suite platform (for example, IVR and speech recognition, inbound and outbound multichannel contact routing, WEM, virtual customer assistants, and analytics). The services need to either be part of a suite of natively built functionality or augmented through technology partners. The platform should include a self-service capability to implement, manage, revise and report on operational performance.

Overall Viability: Several cloud service providers have yet to achieve profitability, as rapid growth and business expansion plans require investment in technology, people and infrastructure to fulfill business growth plans. Many CCaaS providers are private entities or business units of larger companies, and thus do not report detailed balance sheets that enable examination of their financial viability. Revenue indications and growth are important factors for this criterion, as is the overall business strategy for success, which is more readily available for assessment.

Sales Execution/Pricing: The market for CCaaS is not close to saturation, so there are plenty of opportunities for continued growth. We expect suppliers to be able to demonstrate better than 10% annual growth year over year, with a good selection of references from large and well-known organizations, including those with more than 750 agents. Cloud services are elastic and licensing terms should reflect this, enabling a customer to scale up and down in line with business requirements. Although minimum commitments to licenses are to be expected, customers should have the flexibility to vary consumption. Usage-based licensing (per minute/per transaction) is a useful addition that is emerging from some providers.

Market Responsiveness/Record: With several new entrants to the CCaaS market taking market share, being an established player in the on-premises market is often not a major advantage in terms of securing new business.

Marketing Execution: CCaaS providers with strong brand awareness tend to win more business than those without. A comprehensive marketing program is important to attract invitations to bid for opportunities. Brand awareness is also key to developing channels with systems integrators, which are less likely to go to market with providers unknown to their customers.

Customer Experience: Developing a reputation for consistently delivering reliable services and a differentiated CX can help suppliers maintain and grow a CCaaS business. This is especially important as customers commit to strategic CCaaS providers for multiple regions, but still expect to be supported in a timely fashion by local support organizations.

Operations: Contact centers provide critical front-office operations, and customers need to be confident that their CCaaS will be supported by talented, experienced and motivated staff. As customers select strategic suppliers for multiregional needs, CCaaS operations will need to be localized.

Enlarge Table

| Evaluation Criteria | Weighting |

|---|---|

|

Product or Service |

High |

|

Overall Viability |

High |

|

Sales Execution/Pricing |

High |

|

Market Responsiveness/Record |

Medium |

|

Marketing Execution |

Medium |

|

Customer Experience |

High |

|

Operations |

Medium |

Source: Gartner (August 2023)

Market Understanding: Understanding the role that a cloud contact center plays in an organization’s customer service and broader CX strategy — and how it relates to other capabilities — is important for success. Market understanding includes anticipation of market consolidation and new competitors, such as CRM players, and knowing how to defend and increase one’s relevance.

Marketing Strategy: Communicating a differentiated strategy in a market where technologies are largely similar is crucial to win mind share. Gartner clients are increasingly asking about using a single provider across multiple geographies, which should be reflected in a CCaaS provider’s marketing strategy.

Sales Strategy: Striking the best balance between direct and indirect approaches to the market is important when the cost of sale can be very high and compensation impacts cash flow. As customers select a strategic provider for CCaaS, providers must balance customers’ desire to deal directly and centrally for contract terms but be managed locally for regional needs. Managing internal conflict between local sales offices is key to developing strategic relationships with customers.

Offering (Product) Strategy: Vendors should be able to demonstrate an approach to product and service development and delivery that highlights industry requirements and the speed at which differentiated or innovative services are added to their platforms. Customer communities will be increasingly important as sources of information to influence product development as vendors scale up their operations.

Business Model: An important criterion is the relevance of the commercial model to how a vendor proposes to use a combination of direct sales and channel distribution to scale the availability of its service. Partners also need recurring revenue, and the model by which they can profitably resell and support CCaaS customers will be key to a CCaaS provider’s success.

Vertical/Industry Strategy: A focus on specific industries or other segments, such as contact centers of a certain size, creates opportunities to increase mind share in key target markets, in contrast to a horizontal, all-encompassing market vision. For CCaaS providers with lower marketing budgets and reduced overall mind share, the best opportunity to compete and win against larger providers lies in a differentiated vertical/industry strategy.

Innovation: This requires the vision to deliver service-differentiating opportunities, through in-house development or collaboration with innovative partners. Providers’ innovations should reflect the future of applications as APIs and marketplace strategies.

Geographic Strategy: A vendor’s strategy for growth outside its home market in order to attract a larger audience is key to meeting the contact center needs of global and multiregional organizations. A CCaaS provider needs a sound geographic strategy to ensure profitable growth.

Enlarge Table

| Evaluation Criteria | Weighting |

|---|---|

|

Market Understanding |

Medium |

|

Marketing Strategy |

Medium |

|

Sales Strategy |

High |

|

Offering (Product) Strategy |

High |

|

Business Model |

Medium |

|

Vertical/Industry Strategy |

Medium |

|

Innovation |

Medium |

|

Geographic Strategy |

High |

Source: Gartner (August 2023)

Leaders are best described as suppliers with strong support for a wide breadth of customer service capabilities, and an ability to serve multinational organizations with local sales and support organizations. Leaders are more likely to serve customers through channel partners and have strong brand recognition, which has resulted in a large installed base or above-average market growth as a result of customer demand. Leaders also benefit from being able to support varying levels of deployment complexity, including integrations with partners through established marketplaces.

Challengers may have large installed bases of customers, but do not necessarily have the brand awareness or adoption level of Leaders. Challengers are often less mature than Leaders in their multiregional market approach, preferring to focus on strengths in a subset of markets. They may have recognized strengths in serving certain customer-size segments or specific vertical markets. But they are also likely to have less-developed product capabilities than Leaders, or to lack marketplace representation.

Visionaries have strong multichannel product and service capabilities and a clear strategy for sales, marketing and business development. They differentiate themselves by adding unique or innovative functionalities and/or delivery capabilities, which gives them some brand awareness in target markets. Visionaries tend to be smaller than Leaders and Challengers overall, and have more limited investment potential for international expansion.

Niche Players may be quite large or experiencing relatively strong growth, but have decided to focus on a particular market opportunity, a specific set of solutions or certain vertical markets. Their products and services may still be undergoing development, or they may rely heavily on partners to complete their service proposition. Niche Players are likely to be either new or relatively recent market entrants, or suppliers that have yet to build a large customer base.

As CCaaS solutions continue to be sold to larger and more complex accounts, client organizations are increasingly consolidating their contact center platforms across multiple regions with a single provider. In this Magic Quadrant, we focus on the ability of providers to address the needs of global organizations by requiring evidence of demonstrable sales, market and operational presence in at least three regions, as defined earlier in this document.

Market consolidation will enable customer service organizations to meet their customer service needs across a breadth of technologies with a smaller number of providers. Over the past 12 months, CCaaS providers have continued to acquire adjacent technology in order to offer a broader suite of capabilities.

The CCaaS market continues to grow at double-digit rates (see Forecast Analysis: Contact Center, Worldwide), driven by two main factors. The first is the ongoing effort to replace premises-based and server-based contact center infrastructure with SaaS-based capabilities. The second is a desire to deliver an agile, elastic capability for the telephone channel, as well as the ability to support digital channels, WEM, and knowledge and insight management. Additionally, the opportunity to reduce the number of vendor relationships for the entire stack of customer service technologies has proven highly attractive. CCaaS providers offer this opportunity as part of a differentiated approach to premises-based technology providers.

Among the drivers of adoption of CCaaS solutions are the desires to better enable customer and agent experiences, increase the availability and efficacy of customer self-service capabilities, and gain advanced insights into customer experiences both within and beyond customer service activities. We would be remiss not to mention the growing excitement around generative AI, large language models (LLMs) and their ability to impact all three of the aforementioned drivers, among others.

At the time of this writing, CCaaS integration of generative AI and LLM technology is primarily limited to conversation summarization capabilities. However, many CCaaS providers and independent software vendors adjacent to this market are actively developing capabilities that promise to address all of the three market drivers and more. This is generating significant hype for the potential operational customer service improvements that these solutions could bring. It is also driving uncertainty around the potential threat to CCaaS vendors’ agent license revenue, should the enhanced capabilities of generative AI and LLM solutions increase automation to the point that automated interactions will reduce the need for customer service agents. While we see this as a potential long-term issue for CCaaS providers, we expect that these enhancements will largely augment agent activities within the five-year planning horizon. In doing so, they will increase CCaaS vendor revenue rather than cause revenue to decline.

Product/Service: Core goods and services offered by the vendor for the defined market. This includes current product/service capabilities, quality, feature sets, skills and so on, whether offered natively or through OEM agreements/partnerships as defined in the market definition and detailed in the subcriteria.

Overall Viability: Viability includes an assessment of the overall organization's financial health, the financial and practical success of the business unit, and the likelihood that the individual business unit will continue investing in the product, will continue offering the product and will advance the state of the art within the organization's portfolio of products.

Sales Execution/Pricing: The vendor's capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor's history of responsiveness.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization's message to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification with the product/brand and organization in the minds of buyers. This "mind share" can be driven by a combination of publicity, promotional initiatives, thought leadership, word of mouth and sales activities.

Customer Experience: Relationships, products and services/programs that enable clients to be successful with the products evaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, service-level agreements and so on.

Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis.

Market Understanding: Ability of the vendor to understand buyers' wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen to and understand buyers' wants and needs, and can shape or enhance those with their added vision.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the website, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling products that uses the appropriate network of direct and indirect sales, marketing, service, and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base.

Offering (Product) Strategy: The vendor's approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature sets as they map to current and future requirements.

Business Model: The soundness and logic of the vendor's underlying business proposition.

Vertical/Industry Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of individual market segments, including vertical markets.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or pre-emptive purposes.

Geographic Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the "home" or native geography, either directly or through partners, channels and subsidiaries as appropriate for that geography and market.

Tác giả: Vietpbx

Nguồn tin: resources.genesys.com

Những tin mới hơn

Call name: Vietpbx call viet pe be ich, this is the way to read, not standard in English. Meaning: Vietpbx is a combine Vietnam and PBX. We put this name because in Vietnam, almost PBX build by the abroad. We build the PBX for Vietnamese with many feature stay focus in Vietnam